Opt out

If you tell us you want to leave the scheme within 1 calendar month (known as the opt-out period), you’ll be opting out of The People’s Pension.

Why was I enrolled?

Auto-enrolment was introduced by the government to encourage people to save for their retirement. Depending on your age and earnings, your employer needs to enrol you into their workplace pension scheme by law.

After being enrolled, you have the option to opt out.

Things to consider before opting out

You’ll be missing out on extra free money

Pension savings are likely to have better returns than bank account savings

Will you have enough money when you retire?

Before you opt out

We offer a couple of quick and easy ways to opt out. But it’s worth considering the benefits of staying before you do. By leaving, you’ll miss out on extra free money paid into your pension pot by your employer and the government and it’s a great way to top up your retirement income. The return on pensions savings is likely better than any savings account your bank offers you and it’s something you can continue to pay into if you leave your current employer.

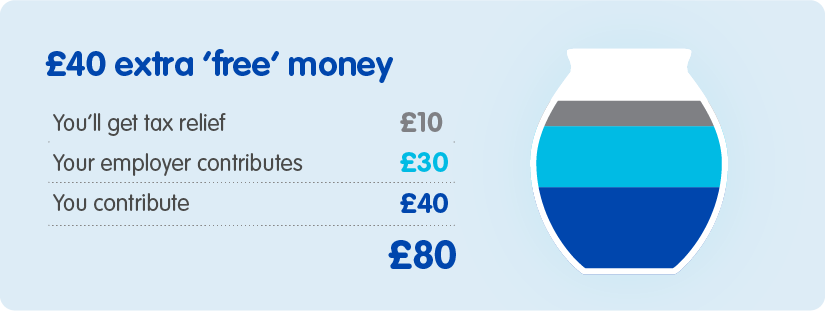

Benefits of paying into your pension potHere’s an example if you were paying in contributions of £40 per month1:

1The example in the diagram above shows what happens when contributions are made after tax, and basic rate tax relief is claimed for you. Higher rate and additional rate taxpayers will need to claim further tax relief through their tax returns. The calculation will differ where contributions are made before tax has been taken and tax relief is received automatically. Find out more about tax relief.

When can I opt out?

You can’t opt out before you’ve been enrolled and received your joiner information. By law, your employer must enrol you even if you’ve said you don’t want to join.

How to opt out

If you do decide you want to leave, you’ll need to have the following to hand:

- your customer number (you can find this on your joiner letter or email)

- your date of birth

- your National Insurance number.

You can either call our automated ‘opt out’ phone service on 0300 330 1280 — or you can tell us you want to leave online.

Opt out online

If you’re sure you want to opt out you can do this online.

Getting refunded

If you’ve been auto-enrolled, you’ll usually have an opt-out period of 1 calendar month from the date you were enrolled to get a refund of your contributions. When enrolled, we send you joiner information either by email or post that tells you when your opt-out period ends.

If you opt out, we credit all refunds back to your employer, who will then give you your refund through their payroll. If you’re still waiting for your refund, it’s best to contact your employer in the first instance.

You can stop active membership after the opt-out period ends but you won’t receive a refund of your contributions. These contributions will remain invested in your pension pot until you take your money. The earliest you can do this is from your normal minimum pension age.

If you’ve been contractually enrolled or you’re an entitled worker, you won’t be able to opt out and receive a refund. However, you can stop active membership. You’ll need to let your employer know, in writing, that you wish to stop your membership and your employer will then need to remove you from the scheme.

Rejoining

If your circumstances change over time, you can ask your employer to opt back in to the pension scheme. You’ll need to submit your request in writing to your employer.

Every 3 years your employer is required by law to put you back into the pension scheme, this is called re-enrolment. If you still don’t want to have a workplace pension at that time, you’ll have the option to opt out again.